I publish Designance sporadically, so you may have forgotten signing up to it. I write it as I explore the principles of design and finance. It’s me thinking aloud as I work out the best way to achieve financial independence. I like to write it long form – ☕️.

Coming up…

Experience: painful lessons in public and private markets 🔥📉 – ⏱ 4min.

I. The pendulum swings

It's been a wild couple of years in "the markets"; first Covid and Quantitative Easing, now inflation and war.

The public stock market began a sustained downward trajectory about 6 months ago and investors have gone from feeling free and easy, to being consciously coy with their capital.

Analysis of a sample of 90 public Software-as-a-Service (SaaS) companies1 shows that 80% now trade at a value below ten times ("10x") the amount of revenue they expect to earn in the next twelve months (NTM). For context, the median peak NTM revenue multiple was 50.8x, down to 8.8x today. An 80% drop.

Closer to home, my shares in Cloudflare have been cut by 75% from their peak. Even my first attempt to "dollar-cost average" (DCA) an investment – that is, buying-in piecemeal over a longer period – couldn't save me from losing over a third (-36%) of the money I originally put in.

Which is fine. It was money I had to burn and a bit of it got burnt. Markets go up, markets go down and (hopefully) even out over the long term.

But, Cloudflare’s still an operational business that's trying to create value:

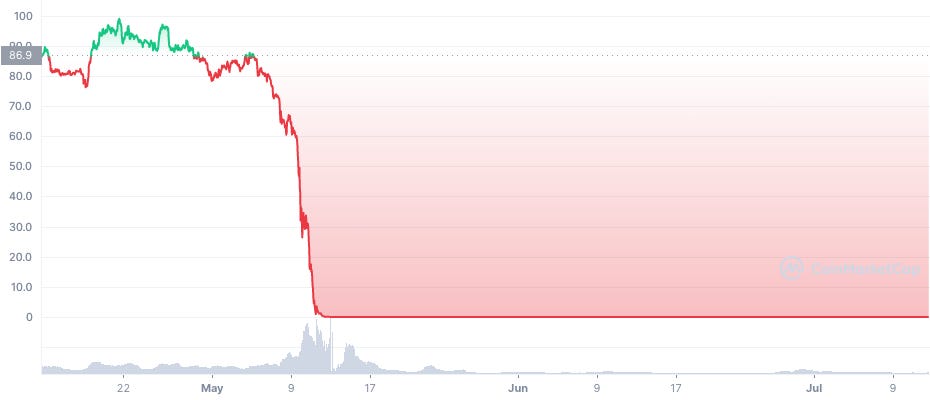

Unlike some crypto… Luna token value:

A chart that shows a -100% loss makes me feel better about my -36% loss.

At its peak, Cloudflare was trading at around 100x its annual revenue. Investors were confident it would grow and make more money (or were happy to wait for 100+ years to get their money back?). Importantly, the inflation-induced correction – or, in this case perhaps, realisation that maybe 100x was maybe a bit overconfident – began creating problems for private companies.

A private company (often) takes investment from private market investors. In return for the risk of investing in (mostly) unproven companies, investors expect a big payout down the line. The public markets usually reward this risk by buying shares at a price far higher than the early investment once the private company goes public.

It's hard (read: expensive) to own a meaningful share of a private company, so you might be thinking "why do I care?". Well, it's surprisingly easy to end up "invested" in a private company; you could be an employee of one.

Private companies that take on investment get that cash in phases; they hit a goal, they get more money. Find a problem; seed funding 💰. Find a solution; Series A 💰. Find more customers; Series B 💰. And so on.

Once these companies have traversed as much as the alphabet as they need to, it's time to raise money in the public market. When the money in the public market gets more skeptical, it puts the onus on the private company to have good "fundamentals". Startups face more scrutiny. Good companies get lower valuations (to match lower expected returns) and the shit ones simply don't make it; their employees end up on layoffs.fyi.

A year ago, a job offer from a startup with a 12 month runway (Ie. how long they can continue to pay their bills for) was fine; it was easy for them to raise more cash later. You probably didn't know if the startup would succeed any better than the next person, but while the money was flowing in no questions asked, it didn't matter; you got paid. If you didn't, well, there was always a new company to jump to.

Today, considering a job offer from a startup requires you to think much more like an investor:

Someone looking for an early-stage startup job is actually in the same position as a savvy derivatives trader" – Byrne Hobart, via The Diff

Ask: is the startup showing signs of promise? Are they building something genuinely valuable? Is a 12 month runway enough? Probably not2. If the company folds, what value can I take to the next job?

Wild bets on companies and ideas with outside odds are being ditched in favour of boring things that make money today.

Bootstrapped businesses are feeling good though; they never needed OPM to get going. They didn’t "shoot for the moon", but they worked hard at solving valuable – often smaller – problems. And they got paid.

Where's the excitement in solving small problems? I guess it's in bootstrapping your own company around them…

I’ve spent the last few months analysing the “applied AI” space. The 2010’s saw the technology sector benefit from the automation of repetitive tasks. My bet is that the 2020’s will deliver the next step-change, beyond the tech sector, using machine learning to build models capable of automating human vision and natural language tasks.

If you want to know how these companies will package, distribute and capture the value of this technology:

Visit ai.roberts.work

Understand more at roberts.work/projects/ai, and

Subscribe to updates at roberts.work/projects

Footnotes

Via 2022 SaaS Crash

The 2008 downturn saw some software companies wait ~3 years before being able to move from survival mode to growth mode